What is the first thing that comes to your mind when you hear the word finance?

For me and most others whom I have interacted with, the answer has been stocks. This is fairly expected given that almost every person whom we know, has heard of or invested in stocks.

Being a PhD student in Mathematical Finance, I have lost count of the number of times I have been asked about suggestions for stocks to invest in for sure profit. Sadly, I wish I knew that myself, then I would definitely be roaming around in my Range Rover somewhere in Swiss Alps! (It’s good to dream 😉 )

On a more serious note, these repeated questions and my own interests in learning more about financial investments, motivated me to write my first series of finance blogs about common alternative sources of investments beyond stocks. While the readers might be familiar with most, if not all of these investment choices, it might still serve as good reminder.

This post will cover the minimal basics of one particular investment choice, namely European call options. I plan to discuss the other investment instruments in details as separate posts in the upcoming weeks. So, without wasting any more time, let’s dive in to the main content.

Options– Having an entire PhD on studying option pricing, hedging and risk optimisation, this had to be my first choice. Options are some of the most beautiful financial instruments there are, owing to their mathematical formulations ( being a mathematician I always try to bring this up 😀 ) and their utility in risk management.

Options fall into the class of financial derivatives which encompass various other instruments. In a less formal language, a financial derivative is a financial instrument whose underlying value is derived from some other asset. If we consider only equity options (equity can be taken as fancy term for stock), then the option’s value (price) is derived from (or dependent on) the underlying equity/stock on which it is written.

Let us understand this with a simple example: Consider Miss Banerjee and Mr Xavier, with Miss Banerjee being the buyer (or holder) of a European call option on an Apple stock from Mr Xavier, who is the seller (or writer) of the call option. This option gives Miss Banerjee the right/option (but not obligation) to buy an Apple stock ten days from today from Mr Xavier at a price of 100$.

This 100$ at which Miss Banerjee can buy the stock 10 days later from Mr Xavier is known as the strike price. The time duration of 10 days is known as the expiry of the option. The price of this option is what Miss Banerjee will pay Mr Xavier to buy the European call option. Let us denote this price by C

Now, Miss Banerjee’s ( the buyer/holder) loss is limited only to what she paid for the option, C. This is because, if at the expiry of the option 10 days later the price of Apple stock is below 100$ (actually below 100 +C $ since she has already invested C to buy the option, but we ignore this for simplicity), she will not exercise the option (not buy the stock from Mr Xavier) since she can easily get it at a cheaper price in the market itself. She only loses C which she paid for the option.

If on the other hand at expiry is higher than 100 ( or 100+C if she wants to also recover the amount C that she paid for buying the option), she has the option to exercise the call option and buy the underlying stock from Mr. Xavier. Again, Miss Banerjee is not obligated or bound to exercise the option. But if she chooses to exercise the option and buys the stock at 100$ from Mr Xavier, she can sell the stock in the market to gain an instantaneous profit. I should clarify here that this a little more subtle since there would be transaction costs for her to sell the stock etc. but we can do not consider that for purposes of simplicity.

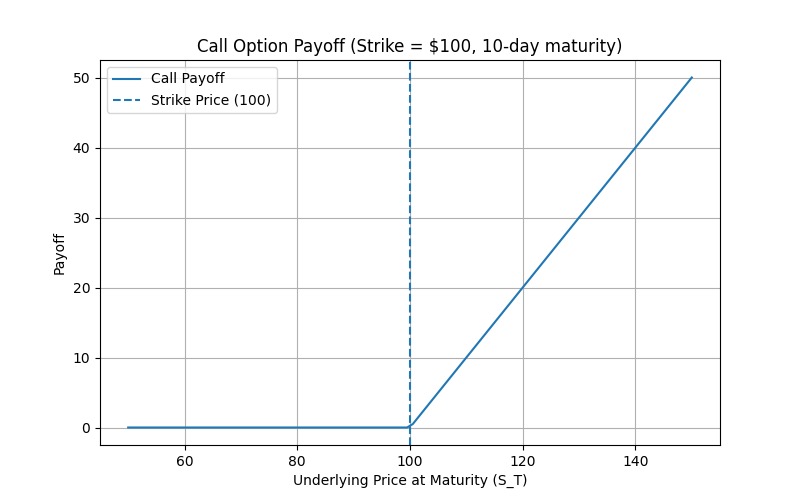

So the payoff for Miss Banerjee ( the buyer or holder of the European call option) at the expiry of the European call option, 10 days from today is, excluding the price C she has already paid for the option :

- Zero, if the stock price is below 100. ( If you include the price C that she has paid, the payoff would be -C in this case)

- S_T – 100, if the stock price is equal to or above 100. Here S_T denotes the stock price at the expiry ( 10 days later). Since she pays 100 to Mr Xavier to buy the stock so it should be deducted to calculate the payoff. (If you include the price C she has already paid for the option, the payoff would be S_T – (100+C) in this case). This S_T can be any value above 100, which makes Miss Banerjee’s potential gain to be unlimited. The plot below shows the payoff for Miss Banerjee excluding C.

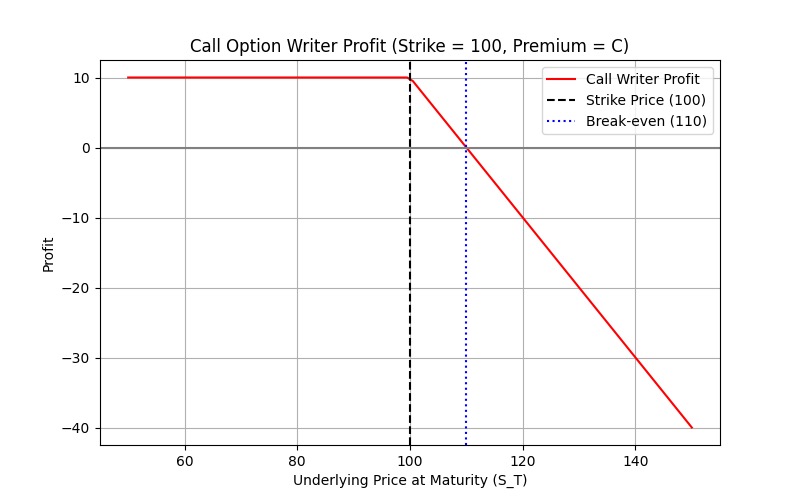

The payoff for Mr Xavier (the seller or writer of the European Call option) at the expiry is:

- C, if the stock price is below 100, since Miss Banerjee does not exercise the call option and will not buy a stock from Mr. Xavier.

- C+100-S, if the stock price is equal to above 100 and if Miss Banerjee exercises the option to buy the stock from Mr Xavier at 100 rupees. In this case Mr Xavier gets 100+C $ from Miss Banerjee in total but has to spend S to buy the stock from the market or forgo the price S which he would have gotten by selling the stock directly in the market. Since S_T can be any value above 100, Mr Xavier’s potential loss can be unlimited. The plot below shows the payoff for the writer Mr Xavier including the amount paid for selling the option, C, with C=10$.

So, seeing these payoffs I hope it is clear why the loss for the buyer (Miss Banerjee) is limited to just C but unlimited for the writer (Mr Xavier).

A put option is exactly opposite in functionality to a call option. It gives the buyer/holder the option to sell a stock at a strike price ( for example 100$) at expiry (for example 10 days) from the seller/writer.

European call/put options are the simplest form of options, also termed as vanilla options. There are several other exotic options like Asian, Bermudan, American, Forward start, Swing options, to name a few. Owing to the complexity of their pricing, I have skipped them in this post.

This payoff structures and complex pricing formulations make options so interesting and risky as well. Hence, financial institutions which sell/write options need to protect themselves from this potentially unlimited risk by hedging. We shall keep this discussion of hedging for another future post.

Hope you liked this post and the explanation. If you did like it, please do comment below. It would be very encouraging for me to keep doing this.

Also, if you have any suggestions for improvements or about topics that you might like me to discuss, please feel free to comment as well.

Until next time,

Purba.

Note: The plots have been generated using ChatGPT.

Resources to read further-

https://en.wikipedia.org/wiki/Option_(finance)

https://www.investopedia.com/terms/o/option.asp

Leave a comment